UPI Transactions : The Zero-Fee Revolution That’s Transforming India’s Payment Landscape

Collage of different UPI transaction revolution payment scenarios – street vendor receiving payment, customer scanning QR code, digital payment apps on phone

Jingling of coins and rustling of currency notes used to reign in the Indian market places. These familiar sounds have now been substituted by a mere beep of a smart phone today. The driving force behind this change is a radical idea that most users are not even aware of UPI transactions revolution are subject to zero merchant discount rate (MDR) charges. This one policy move has transformed the way more than 1.4 billion Indians manage money in their day-to-day lives.

Chapter 1: Get to Know the Game-Changer

![]()

Division picture between conventional cash transaction and UPI QR code payment

So What is Merchant Discount Rate?

But first, what is Merchant Discount Rate in simple terms before we indulge in the revolutionary method offered by UPI transaction revolution? Consider that you own a small grocery store. Whenever a customer uses credit or debit card to make payment, the bank debits your account a small percentage of the amount paid. This fee is Merchant Discount Rate or MDR.

To illustrate, when a customer purchases groceries amounting to ₹1,000 through a credit card, and the MDR is 2 percent, you as the merchant would pay 20 rupees to the bank to process the transaction. although 20 rupees may not be a big deal, consider the case where you are a small tea vendor whose tea is priced at 10 rupees a cup. A MDR of even 1 per cent would result in you losing ₹0.10 on each digital transaction, which is huge when your profit margins are already slim.

The UPI Revolution: Zero becomes the Hero

![]()

Infographic of 0% MDR with UPI logo and other payment applications

At the launch of UPI (Unified Payments Interface), the government took a very ambitious call: all UPI transactions revolution will be completely free of charge to the merchants. Zero rupees. Zero paise. It was not a limited time promotion offer but it was adopted as a permanent feature and would make everything different.

This move was a game changer since it eliminated the greatest obstacle that hindered the adoption of digital payments among small businesses. In a sudden turn of events, the vegetable seller in the neighborhood, the barber in the local shop, the street food vendor, and everyone else in between could take digital payments without the fear of losing money on every sale.

Chapter 2: The Path to UPI

Infographic of the timeline of the evolution of cash to cards to UPI

The Age of Cash-in-Charge

India has remained a high cash economy. Over decades, physical money ruled. Men walked around with thick wallets and pockets loaded with coins. Cash was favored by the small businesses since it was instant, did not involve any technology, and had no accompanying fees.

But cash had its own troubles:

- Threats of security when walking with a lot of money

- Problems with making change accurately

- Tedious counting and checking up

- Danger of false notes

- Difficulties of keeping books of accounts

- The Card Payment Challenge

The picture depicts an array of credit/debit cards and a POS terminal

The convenience and the security were the selling points when credit and debit cards were introduced in India. To the customers, cards were truly convenient – they did not have to carry cash around, it was easier to monitor expenditure and it was safer compared to carrying lots of money.

However, cards had one huge disadvantage to merchants, and particularly small merchants; the MDR fees. These fees were usually between 0.4 percent and 2 percent of the transaction amount depending on the card type and the merchant category.

How did these charges impact businesses of various kinds? Let us see:

Big- box Stores: Large retailers were able to cover these expenses due to their huge sales and profit margins. To them, the convenience of digital payment was more than the MDR charges.

Medium Businesses: Restaurants, cloth shops, and electronic stores found it comfortable but tended to like cash payments in smaller bills to avoid charges.

Small Businesses: The difficulty really consisted. A small tea stall that earns 10 rupees a cup could not absorb a loss of 0.20 rupees per card transaction. Lots of them just did not accept cards or set minimum purchase amounts.

The Online India Drive

![]()

Digital India logo and other symbols of digital payment methods

The Digital India initiative was a government program that was meant to make the society digitally empowered. But the MDR fees of the card transactions were already forming a serious obstacle to this objective. Small merchants were also hesitant to accept digital payments and customers had to deal with the inconvenience of being requested to pay in cash even for small values.

This had to stop and it did in the shape of UPI transaction revolution.

Chapter 3: Zero-MDR Masterstroke of UPI

Infographic containing the UPI architecture consisting of banks, NPCI, and payment apps

The Daring Move

When the National Payments Corporation of India (NPCI) was working on UPI transaction revolution, they had a major choice to make regarding fee structure. They would have been justified to take the conventional route of making money by charging merchants per transaction, yet they decided to take the radical approach that can be summarized as zero MDR on UPI transactions.

This choice was grounded on a number of strategic factors:

Financial Inclusion: Eliminating the cost of transactions on the merchant side, UPI transaction revolution would make even small merchants accept digital payments, moving them into the formal financial system.

Volume Over Fees: The idea of making money out of transaction fees was abandoned, and it became serious about creating a huge digital payment ecosystem that would make the whole economy benefit.

Rivalry with Cash: In order to compete with cash genuinely, merchants had to be indifferent about the cost of digital payments. This was achieved by Zero MDR.

Zero MDR in Practice

![]()

Schematic demonstration of UPI transaction revolution involving customer, merchant and banks

This is what happens at the background when you make a UPI payment:

- Customer starts payment: You scan a QR code or type in a UPI ID of a merchant

- Transaction Request: your payment app submits the request to your bank

- Bank Processing: Your bank takes the payment and moves money to the bank of the merchant

- Settlement: The money is deposited into the account of the merchant

- Zero Charges: The merchant does not pay anything in the course of this whole process

This can be compared to a card transaction in which the merchant would part with a percentage of the transaction value to different parties that are involved in the payment processing.

Chapter 4: Stories in the Real World

Collage of different small entrepreneurs consumers of UPI – vegetable seller, auto Rickshaw driver, street food vendor

The Transformation of the Vegetable Vendor.

This is Ramesh, a vegetable seller at Dadar market in Mumbai. Publishing before UPI transaction revolution, he transacted purely in cash. Customers would also have a problem with giving exact change and he would need to maintain a lot of cash in the business which was risky.

Ramesh says, “I was reluctant when UPI arrived. I expected some charges like in card machines. Everything changed when I found out I would not have to pay any fees. One can now pay digitally even to buy ₹20 worth of goods. This has improved my sales as customers are not anxious about getting the correct change.

The story of Ramesh is repeated millions of times in India. Small sellers who could not believe that they would ever be able to afford digital payment methods proudly show their QR codes now.

The Tea Stall Revolution.

Picture of a conventional tea stall with UPI QR code

Suresh is a tea seller outside an office in Bangalore. His average cup of tea is 15 rupees. With UPI transaction revolution, accepting card payments are impossible – the MDR fees will nibble into his already thin profit margins.

Through UPI, Suresh says that he is not losing even a rupee on online payments. The convenience is appreciated by office workers and I do not have to worry about making change or counting cash at the busy times. This has increased my business since customers pay with ease.

The Digital Journey of The Rickshaw Driver

Auto-rickshaw including UPI payment sticker

UPI payments have been adopted by auto-rickshaw drivers in cities of India. The zero MDR feature is crucial to them especially since their incomes are meager and every rupee matters.

Kumar, an auto driver in Delhi, states, “Previously, passengers used to dispute the change, particularly small quantities. They now only need to scan and pay. I am given the fare exact without deductions. It has simplified my life a lot.”

Chapter 5: Economics of Zero MDR

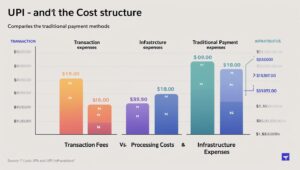

Infographic on UPI and the traditional payment methods cost structure comparison

Who pays the price?

The operational costs in case merchants do not pay MDR on the UPI transactions revolution? The solution is in another economic model:

Government Subsidy: The government at first subsidized the zero MDR model as it was seen as an investment in digital infrastructure.

Bank Infrastructure: The processing costs are incurred by the banks as a larger digital strategy and gain customers engagement and data benefits.

Volume Economics: The sheer size of the UPI transactions revolution provides economies of scale, and thus, makes the individual transaction processing less expensive.

Ecosystem Benefits: This is a value generated in the entire digital ecosystem because of the additional volumes of transactions, which subsequently subsidizes the direct costs of transactions.

The Long-Term Strategy

![]()

Chart illustrating the increase in the UPI transactions over time

The zero MDR policy was not only about instant adoption, but a long term plan to develop India digital payment infrastructure. With the cost being eliminated as a factor, UPI might accomplish:

- Quick Adoption: Merchants would not have second thoughts about digital payments

- Network Effects: The more merchants adopted UPI transaction revolution the more customers would utilise it

- Data Generation: The higher the digital transactions, the better economic data would be generated

- Financial Inclusion: Small businesses would be included into the formal financial system

Chapter 6: UPI Vs Global Payment System

The world map with the locations of various payment systems and their fee structure

International Perspective

The majority of the nations impose MDR on online payments. How does UPI transaction revolution fare in comparison:

United States: The cost of credit card processing varies between 1.5 % and 3.5 % of the transaction amount. Small merchants tend to either pass the costs to the consumer or impose minimum transaction limits.

European Union: In the EU, interchange fees have been capped at 0.2% on debit cards and 0.3% on credit cards, however the merchants do pay processing fees.

China: Alipay and WeChat Pay merchants are between 0.1% to 1% depending on the type of transaction and the category of merchants.

Singapore: The instant payment system adopted in Singapore, Pay Now has low fees, although UPI transaction revolution with its zero-fee model is more merchant-friendly.

What is special about UPI?

Comparison chart UPI vs other payment system

UPI is unique in the world since:

- Zero Cost Complete: Unlike other systems that have lowered charges, UPI transaction revolution has removed it altogether on the part of the merchants.

- Universal Acceptance: UPI transaction revolution payment can be accepted by any business, small or big without any cost consideration.

- Government Support: Zero-fee sustainability supported by the powerful policy support.

- Interoperability: The UPI infrastructure can be shared by several apps

Chapter 7: The Ripple Effects

Schematic illustration of some of the sectors impacted by the adoption of UPI

Effect on Other Industries

Retail and Commerce: The small and medium retailers have adopted digital payments. The cash-only street markets are abuzz with the sound of the UPI payment confirmation.

Transportation: UPI transaction revolution can be used to pay auto-rickshaws and taxis and even local buses. This has eased the transport system both to the drivers and passengers.

Food and Beverage: The food industry, whether it is a five-star restaurant or a food stall by the road, has adopted UPI hugely. This trend has also been enhanced by food delivery apps.

Healthcare: Healthcare professionals, health centers, and drugstores accept UPI transaction revolution as payment to cover consultation costs and the purchase of medications, which makes the payments in the healthcare system more traceable and transparent.

Education: Schools, colleges and coaching centers are also receiving fee payments through UPI transaction revolution which otherwise would have been a bulky amount of cash.

Social and Economic advantages

Infographic of benefits such as financial inclusion, less black money etc.

- Financial Inclusion: Previously unserved millions of small businesses have been brought into the formal financial system, and have digital records of their transactions that can facilitate their getting credit and insurance.

- Black Money less: With digital transactions, there is a trail of audit, and thus it is difficult to conceal income and avoid paying taxes.

- Enhancing the collection of Tax: The government is also in a better position of monitoring the economic activity and making sure that taxes are paid accordingly.

- Enhanced Security: Businesses cash handling is reduced which decreases risks of theft and robbery.

- Improved Record storage: Electronic transactions result into automatic financial records that assist businesses in management of their accounts.

Chapter 8: Problems and Recommendation

The Challenges

Although zero MDR model has been successful, it has a few challenges:

- Sustainability Concerns: Skeptics also wonder how zero fees can be maintained in the long term, and whether fees will be Ultimately, introduced.

- Infrastructure Costs: There must be someone who pays to maintain the digital infrastructure and that someone is now the banks and the government.

- Competition with Conventional ways: Even though the use of UPI transaction revolution has expanded at a fast pace, cash transaction continues to prevail in several areas and industries.

Solving the Concerns

- Government Commitment: The government has several times promised not to make UPI transactions revolution free to merchants, considering it as digital infrastructure.

- Creative Business Models: Rather than transaction fees, the ecosystem is looking into other revenue generation such as value-added services, analytics, and lending products.

- Continuous Innovation: UPI transaction revolution is getting new features and capabilities to make it more valuable than a simple payment processor.

Chapter 9: Stories of Success around India

![]()

India map with the icons of success stories in various states

Rural Transformation

UPI transaction revolution has also introduced digital payments in rural locations where it was nearly impossible to accept cards because of MDR issues.

Village Markets: UPI transaction revolution is getting widespread use in weekly village markets (haats). The farmers who sell vegetables, grains, and other products do not hesitate to receive digital payments without thinking about the cost of transactions.

Agricultural Transactions: The farmers who get money in exchange of their farm productions can now be paid electronically to improve their financial records and to eliminate the risks associated with cash.

Urban Evolution

Market place in the city with multiple UPI payment scenarios

In cities the changes have been still more dramatic:

Culture of Street Food: Popular street food spots such as Mohammed Ali Road in Mumbai, Chandni Chowk in Delhi, or Park Street in Kolkata rely heavily on UPI transaction revolution at this point.

Local Services: Be it barbers, tailors, electricians, plumbers, UPI transaction revolution has been embraced by all local service providers, which have made neighborhood business easily transacted.

Cultural Events: Even the religious donations in temples, gurudwaras, and churches are now being collected through UPI transaction revolution, and zero charges mean that more money will go to the intended cause.

Chapter 10: Zero MDR Technology Index

Technical scheme UPI infrastructure

The Infrastructure

The capability of UPI transaction revolution to support zero MDR is due to its optimized technological framework:

Centralized Processing: The centralized system of NPCI abolishes several intermediaries and makes the processing cheap.

Standardized Protocols: The similarity of technical standards in all apps that enable UPI transaction revolution lowers complexity and expenses.

Government Support: The policy support and the start-up funding assisted in putting in place the infrastructure without the direct demand on revenue.

Payments Processing Innovation

![]()

Flowchart: The UPI transaction revolution processing

UPI was the first to introduce a number of innovations:

Direct bank-to-bank transfer: UPI transaction revolution enables banks to transfer money directly, unlike card networks, which entail the involvement of additional parties.

Real-Time Processing: The real-time settlement lowers the transaction delay cost and reconciliation cost.

Unified Interface: One interface to all banks and payment service providers simplify operations.

Chapter 11: Recognition throughout the World and Future

UPI wins international attention

International Acclaim

The zero MDR model announced by UPI transaction revolution has attracted worldwide attention:

Recognition by World Bank: UPI transaction revolution has won accolades and compliments from the World Bank as being an example to other developing nations.

International Adoption: Other nations are examining the structure of UPI transaction revolution to adopt the same.

Interest of Tech Industry: International technology corporations are teaming up with Indian corporations to bring UPI-like systems to the global markets.

Future Developments

Scenarios of the future of payments – voice payments, IoT payments, etc.

The zero MDR base lets things get exciting in the future:

Voice-Based Payments: Talking payment commands can be as widespread as QR code scanning.

IoT Integration: It might also involve the automatic processing of payments without human involvement that is made possible by Internet of Things devices.

Cross-Border Expansion: UPI transaction revolution is also being introduced to the global markets, and it will continue to follow its affordable trend.

Blockchain Integration: Subsequent releases may use blockchain to enable better security and transparency.

Chapter 12: Business and Consumer tips

Divided picture with business tips on one side and consumer tips on the other side

For Businesses

Getting Started:

Reach out to your bank to have UPI merchant services enabled

Show your QR code in a visible place

Educate employee on how to process UPI transactions revolution

Have secondary means of payment at hand

Best Practices:

Rec reconciling UPI transactions revolution on a regular basis

keep account of transactions in accounting

Enlighten the customers on UPI payment

Save on zero MDR and use it to better the quality of service

For Consumers

Maximizing Benefits:

Encourage merchants by using UPI in every transaction that is possible

Store several UPI apps as backups

Before payments, check merchant particulars

Save receipts of transactions on warranty and returns

Safety Tips:

You must never provide your UPI PIN to anybody

Check payments figures prior to authorizing

Only official payment apps can be used

Report suspicious transactions on time

Chapter 13: The wider economic effect

Infographic with the macroeconomic effects of UPI transaction revolution

Macroeconomic Benefits

- GDP Growth: The growth in the volume of digital transactions is a contributor to the indicators of economic activity and GDP growth.

- The health of the Banking Sector: Banks gain more customer interactions and digitalization, even taking into consideration that they cover UPI transaction revolution processing fees.

- Government Revenue: Enhanced tracking of the transactions means enhanced tax collection and compliance.

- Investment Attraction: The developed digital payment system is the reason India is a magnet to foreign investments in fintech and associated areas.

Microeconomic Changes

![]()

Small business owner looking at UPI transactions revolution on the phone

- Empowerment of Small Business: Small businessmen are now able to compete with bigger companies when it comes to providing convenient payment terms.

- Consumer Behavior: Consumers are more comfortable to make smaller digital purchases, which increases consumption trends.

- Improvement of Cash Flow: Payments to businesses are made immediately, which helps in management of cash flow.

Chapter 14: Resolving Today s Popular Worries

FAQ-based design containing popular questions on UPI MDR

Will UPI Always Be Free to Merchants?

This is the most widespread objection. The government and NPCI have continuously sticks to their decision of zero MDR on UPI transactions revolution. The policy is considered as a basic digital infrastructure, just as roads or electricity are delivered.

How Do Banks Make Money through UPI transaction revolution?

Here are some of the ways in which banks gain through UPI transaction revolution:

- Enhanced customer out reach and analytics

- The possibility of cross-selling of other financial products

- Lower costs of handling cash

- Increased customer loyalty

Is UPI Safe to use in Big Transactions?

Transactions using UPI are enforced with several levels of security:

- Bank-grade encryption

- Two-factor authentication

- Adjustable transaction limits

- Fraud monitoring in real time

What If the Internet Goes Down?

Although UPI needs an internet connection, Indian digital infrastructure has become resilient. Additionally:

- Various connection possibilities (WIFI, mobile internet)

- Developing offline payment capability

- Alternate payment methods should always be advised

The Zero-Fee Revolution Is Still On

Making the move to abolish the merchant discount rates on UPI transactions revolution is one of the biggest policy innovations in the world of digital payments. The apparent trivial decision to introduce zero fee to merchants to accept digital payments has revolutionized the economy of India in a way that is still developing.

Whether it is the large tea vendor who no longer has to fear transaction costs or the technology startup that develops new payment technologies, the zero MDR policy has opened an ecosystem where digital payments actually compete with cash on a level playing field. The ripples are still going across all sectors of the economy.

With India transitioning into a full digital economy, the zero-fee structure established by UPI transaction revolution offers a solid basis of innovation and development. The experiences of this model provide helpful insights to policymakers across the world that are struggling with the challenge of ensuring digital financial inclusion and sustainable business models.

The history of zero MDR at UPI is, in the end, a history of elimination: elimination of obstacles, which did not allow small merchants to accept Digital payments, eliminated hesitation among customers to go cashless, and eliminated financial exclusion. By bringing down these barriers, India has been able to build a digital payment system that is inclusive of all whether it is a big corporation or a small street vendor.

The zero-fee revolution has just begun. The notion of ensuring that digital payments remain affordable to every player is one principle that has steered the growth of digital payments in India as new technologies come up and new use cases are discovered. In an era when every percentage point of transaction charges can make a difference to small companies working on small margins, the zero MDR policy of UPI transaction revolution can be seen as a ray of inclusive innovation.

It is not merely a payment system but a reimagination of what digital infrastructure can do to benefit the society. India has created a digital payment network that is truly common property of all the citizens of the country, by prioritizing the common good over the short term revenue earning potential. The effectiveness of this strategy provides inspiration and directions to other similar efforts around the globe that it is possible to have technology that is advanced and all-inclusive, effective and fair.

We are involved in this silent revolution – scanning QR codes and finalizing transactions with just a tap on our phones have made digital payments as easy to use as cash, yet more transparent, secure and convenient. The zero-fee promise of UPI transaction revolution is being realized, transaction after transaction, merchant after merchant, making India a digital-first economy, where anyone can easily be a part of it without the fear of any hidden fees and restrictions.

Written by : Nitasha chauhan